Regulatory update: New Overseas Funds Regime European Long-Term Investment Funds

Two major regulatory changes have been announced this month for EU and UK based asset managers:

- The new Overseas Funds Regime is a major opportunity to win business in the UK. It allows overseas investment funds to apply to become recognised in the UK and marketed to UK investors.

- The European Commission has also published its regulatory technical standards for European Long-Term Investment Funds. These now more power over liquidity management into the hands of asset managers in both EU and UK.

Overseas Funds Regime

Taken together, these sought-after changes will streamline and improve processes whether related to a post-Brexit environment or navigating long term investment funds in Europe.

The new Overseas Funds Regime (OFR) re-opens the UK market for funds which were not registered under the Temporary Permissions Regime (TMPR). The new regime – announced in May and updated in July – allows overseas investment funds to apply to become recognised in the UK and marketed to UK investors.

As the UK government points out, the majority of the funds currently able to market to UK retail investors are based in the EEA. The OFR ensures UK investors will continue to benefit from the choice these funds provide, with the assurance that they come from a country with equivalent consumer protections.

Since the TMPR closed in 2020 many new funds have effectively been locked out of the UK market and asset managers have been waiting for a more practical solution for UK fund distribution to professional and retail clients. The OFR creates the right framework to meet these demands.

The FCA published additional guidance in July with the new regime becoming effective for funds not registered under the TMPR in September 2024. We expect there to be significant pent-up demand looking to access the market under the new regime.

For those funds registered under the TMPR landing slots will become available to register under the new regime from October 2024 for stand-alone funds and from November 2024 for umbrella funds. Umbrella funds will be allocated landing slots alphabetically based on the name of their “operator” (UCITS Management Company or AIFM). The TMPR will cease in December 2026 and funds who miss their landing slot will have their access to the UK market revoked.

It is important that asset managers begin preparations now, to ensure they successfully navigate the application review process.

For those funds operating under the TMPR, the FCA will issue a ‘direction’ to each fund operator, 8 weeks prior to the fund operator’s landing slot opening, telling the fund operator how to apply. Carne’s landing slot is currently scheduled to be in March 2025.

European Long-Term Investment Funds

The European Commission has published its regulatory technical standards for European Long-Term Investment Funds (ELTIFs) – placing more power over liquidity management to private asset managers.

The democratisation of private markets isn’t a new theme, but new policies and fund structures are making access simpler than ever. We have already seen more closed-ended ELTIF 2.0s being launched – and with defined contribution (DC) pension schemes and wealth managers planning to considerably increase allocations to private assets, according to our new research1 , we expect to see a lot more demand for these products

The Regulatory Technical Standards (RTS) do not mandate a minimum notice period for redemptions. However, the ELTIF manager must set a maximum redemption size using one of two methods outlined in Annex I or Annex II of the RTS. This determination considers the total UCITS-eligible assets at the redemption date and a 12-month forecast of expected cash flows, excluding new subscriptions.

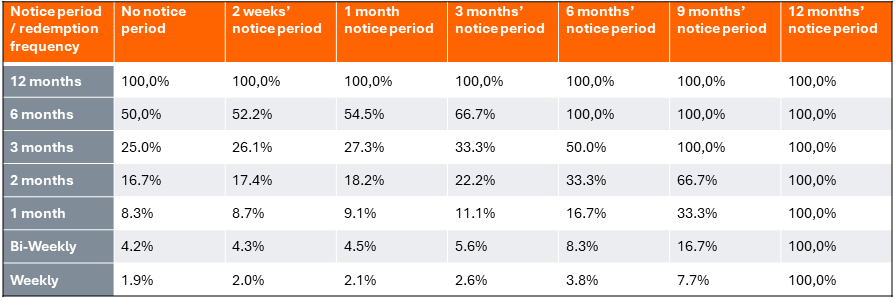

Annex I: The maximum redemption size depends on the redemption frequency and notice period. A longer notice period allows a higher percentage of UCITS-eligible assets to meet redemptions. It also offers flexibility to aggregate redemptions over one or two months.

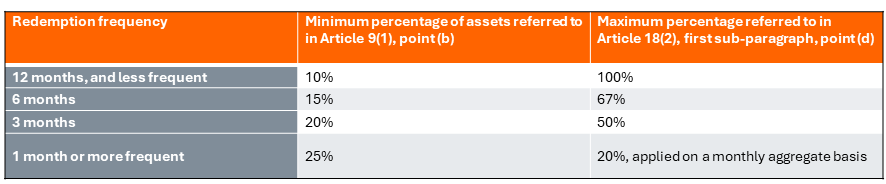

Annex II: The maximum redemption size is tied to the redemption frequency and a required minimum percentage of UCITS-eligible assets. A longer redemption frequency permits a higher percentage of these assets to be used for redemptions.

ELTIFs must follow specific liquidity management rules. They can use redemption gates if liquid assets are insufficient for redemptions, must set a minimum holding period for open-ended funds, and notify any significant changes to redemption policies to national authorities one month in advance. AIFMs can select from a full range of liquidity management tools in the revised AIFMD, not just specific options like anti-dilution levies, swing pricing, and redemption fees.

Based on conversations with clients and our data, we expect a marked increase in the take-up of ELTIFs.

Please contact us if you would like to discuss OFR or ELTIFs with one of our regulatory solution experts.

Canopy

Change 2025: Embracing evolution – Siobhan Noble, Managing Director

CG Aegon AM Private Credit LTAF receives FCA approval

IWD 2025: What we learned and why it matters

Change 2025: Going for growth – Glenn Thorpe, Managing Director